Key Messages

- Risk must be taken in the right order. Growth constraints come before allocation decisions.

- Risk capacity is an economic boundary — softer than regulatory capital, but harder than portfolio preferences. It is defined by cash-flow funding, stress survivability, and avoidance of forced liquidation.

- Exposure management creates value only within constraints. Allocation matters only after admissible growth paths are established.

- Fragmentation destroys coherence. When balance-sheet steering and exposure decisions are disconnected, value erodes silently.

Why portfolios fail in practice

Most insurance portfolios do not fail because too much risk was taken.

They fail because risk was taken in the wrong order.

Some portfolios look diversified, yet struggle when inflation accelerates or liquidity tightens.

Others remain solvent for decades, but consume far more capital than their economics justify.

In almost every case, the underlying tension comes down to two questions that are too often blurred:

- How much risk can this system really carry over time?

- And where should that risk be deployed so it creates value rather than fragility?

These questions point to two different kinds of discipline.

They are not substitutes. They are orthogonal.

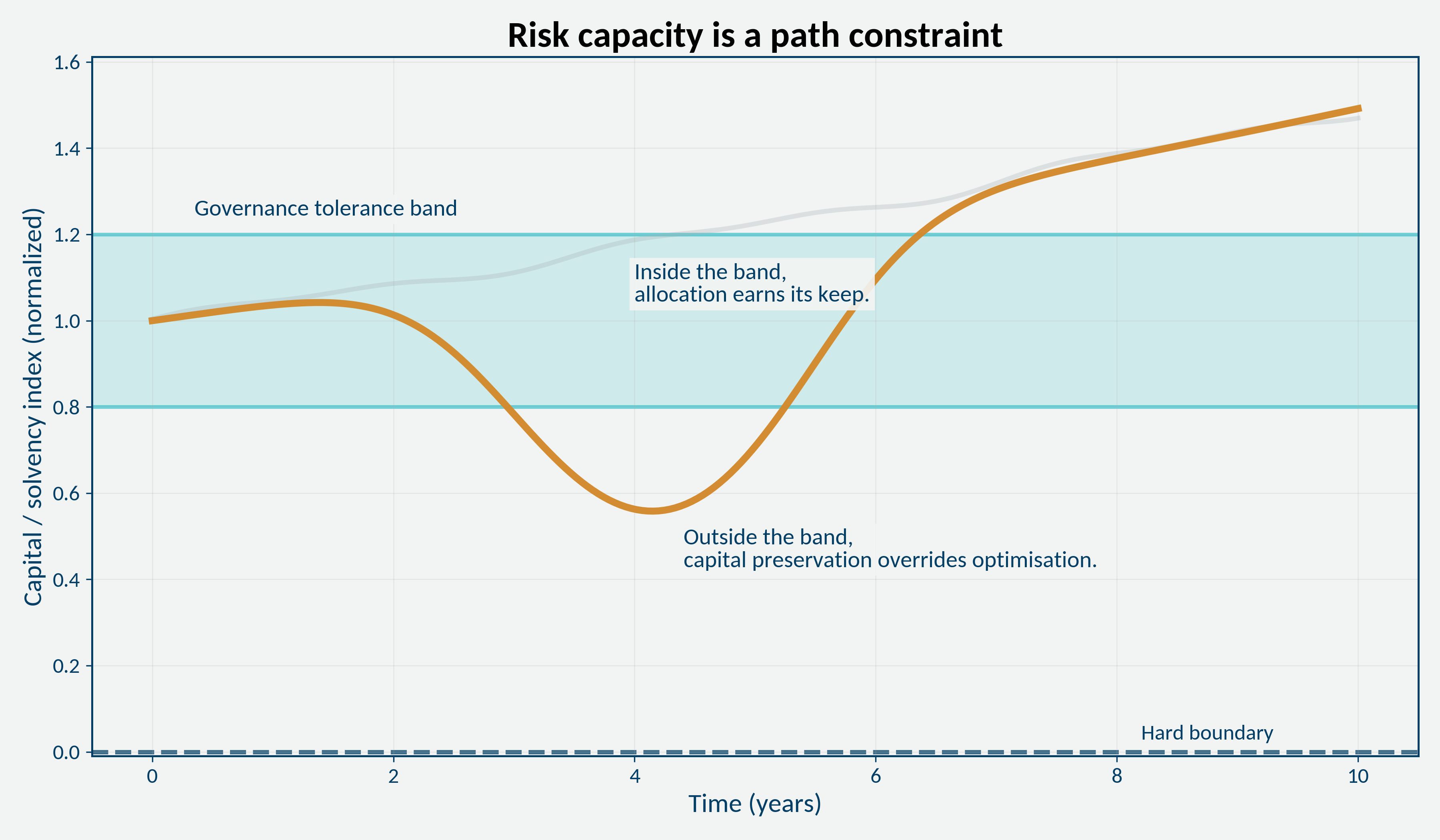

How much risk can the balance sheet really carry?

Every insurance system has a limit — not just a regulatory one, but an economic one.

Cash flows must be funded.

Assets must survive stress.

Capital must absorb volatility without forcing the wrong decisions at the wrong time.

That problem shows up in balance-sheet steering, i.e. Asset & Liability Management (ALM).

This is where thinking about risk capacity matters: whether asset cash flows can fund liability cash flows, whether financial market stress can be survived, and whether growth paths avoid ruin or forced liquidation. These constraints determine how aggressive the system can be, how much drawdown it can tolerate, and how close to the edge it can operate.

Risk capacity does not arise in isolation. It is the output of a coherent ALM system — one that integrates capital, liquidity, accounting, and funding into a single steering logic. Without this system, risk capacity becomes unstable, stale, or distorted, and exposure decisions lose their economic meaning. Only once the ALM engine defines admissible growth paths does exposure management become a value-creating discipline rather than a defensive one.

Where risk capacity actually creates value

Once risk capacity is understood, a different tension appears — and it is no longer a balance-sheet problem.

It is a portfolio problem.

Given a fixed risk budget:

- Which exposures deserve it?

- Which ones quietly dominate the loss distribution?

- Which ones add value because they diversify and pay for the risk they bring?

This is where exposure management lives — best understood as portfolio thinking applied to capital-relevant risk, not abstract return optimization.

Individual risks are allowed to be ugly.

Portfolios are not.

With risk capacity fixed, the question shifts from how much risk to take to where it should sit in the portfolio.

.png)

Why diversification alone is not enough

If exposure decisions were only about reducing risk, the optimal portfolio would be trivial:

- infinite diversification,

- minimal exposure,

- no economic relevance.

Real exposure decisions do the opposite.

They concentrate risk where it is paid for, and avoid it where it is not.

That requires looking at:

- marginal contribution to tail risk,

- interaction effects between exposures,

- value density per unit of scarce risk capacity.

This is why exposure management is uncomfortably close to value management — not because it ignores risk, but because it refuses to ignore where risk actually shows up in the distribution.

Why P&C and Life learned different lessons

Historically, insurance lines evolved under different dominant uncertainties.

Property & Casualty insurance grew around:

- short-term contracts,

- annual repricing,

- event-driven, heavy-tailed losses.

Aggregation was the problem. Exposure discipline matured naturally.

Life insurance grew around:

- long-term guarantees,

- locked-in economics,

- sensitivity to discounting and reinvestment.

Time was the problem. Balance-sheet steering matured naturally.

This split was not cultural. It was structural.

What breaks when one axis is ignored

Trouble starts when one dimension is managed in isolation.

P&C portfolios without strong balance-sheet discipline tend to discover:

- pricing that silently assumes benign inflation,

- liquidity stress after loss years,

- capital erosion driven by timing rather than aggregation.

Aggregation is controlled — but the trajectory is not.

Life portfolios without strong exposure discipline tend to suffer from:

- concentrated guarantees,

- capital locked into low-value risk,

- limited ability to reshape legacy books.

Time is controlled — but risk density remains opaque.

In practice, these failures rarely appear as dramatic breakdowns. They surface gradually — as pricing surprises, unexplained capital strain, or uncomfortable questions that never quite get resolved.

Organizational lens

What makes these failures persistent is rarely a lack of models.

More often, it is a lack of organizational coherence.

Exposure decisions, capital policy, pricing assumptions, and balance-sheet steering typically sit in different parts of the organization, each optimized locally and defended rationally. Aggregation is managed in one place, funding assumptions in another, and capital constraints somewhere else entirely.

The result is not reckless risk-taking, but structural incoherence: a portfolio that makes sense in pieces, yet fails to behave as a system when stress arrives. Each function is locally right — and the portfolio is globally wrong. In practice, insurance risk does not fail along a single dimension.

Across exposures, the question is how risks interact at a point in time.

Across time, the question is how the balance sheet evolves under stress.

Neither can substitute for the other.

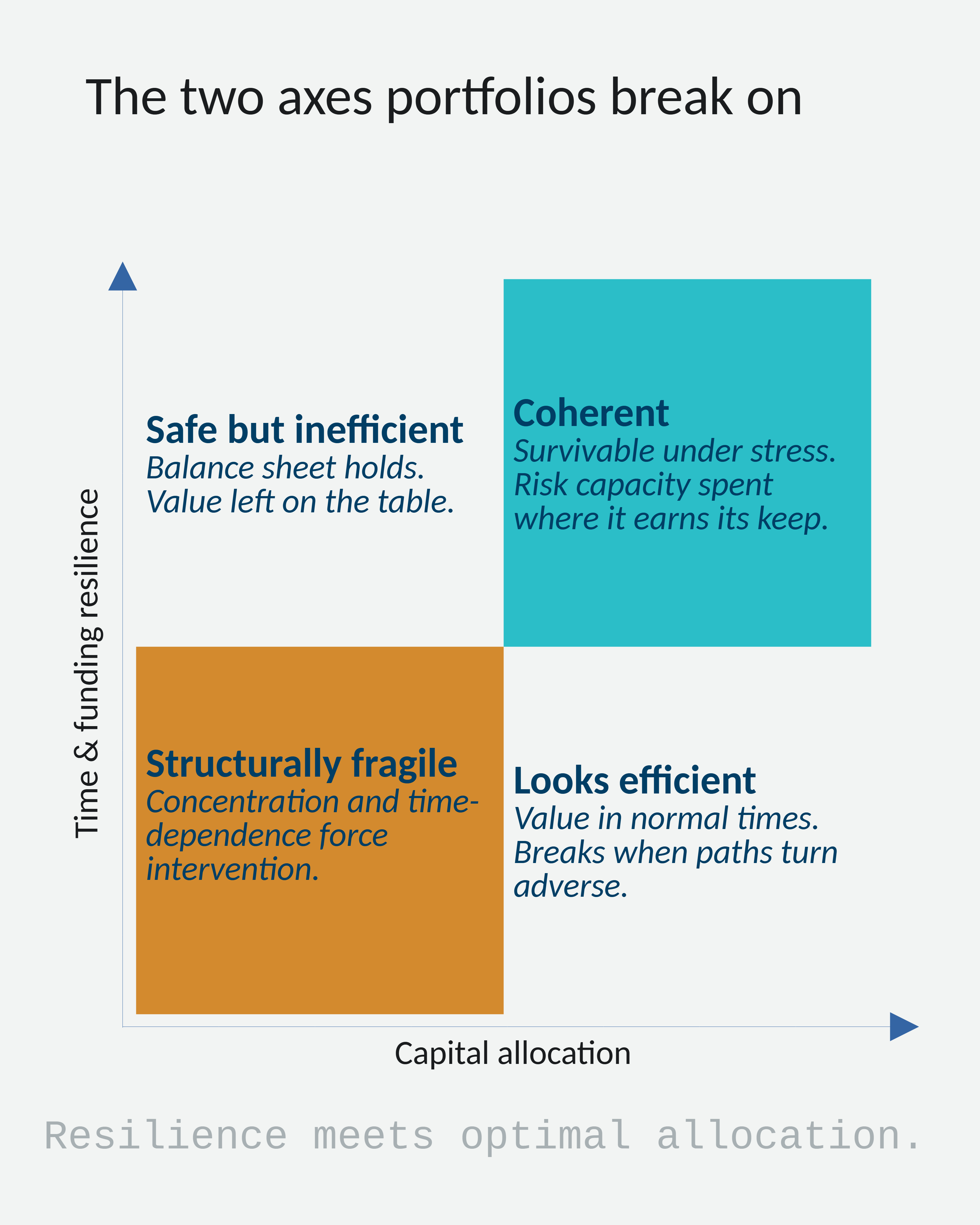

What a complete risk system looks like

Exposure discipline without balance-sheet thinking creates hidden fragility.

Balance-sheet discipline without exposure thinking creates hidden capital inefficiency.

The only takeaway that matters

No individual risk needs to be safe.

But the portfolio must be survivable,

and risk capacity must be spent where it earns its keep.

In practice, improving insurance risk performance is less about better models, and more about aligning risk capacity, exposure decisions, and governance into a single, coherent system.

Tags: risk, insurance, alm, exposure-management, portfolio-thinking, capital-management