Key Messages

- Outcomes differ because systems differ. Success in ALM is not about expert teams, but about whether the organisation operates as an integrated system.

- Fragmentation destroys value silently. Misaligned risk, treasury, capital, pricing, accounting and investment functions create hidden frictional costs and deteriorating capacity.

- ALM is a strategic engine, not a reporting function. When designed intentionally, it coordinates constraints, economics, liquidity and solvency into one steering logic.

- Integrated ALM creates capacity, discipline and clarity. It enables better pricing, more stable earnings, improved growth decisions and transparent risk–return profiles.

- A modern ALM system must be timely, connected and economically grounded. This article outlines how such a system is structured and why it matters.

In my career, I have seen what it takes for deals to succeed, for risks to be absorbed cleanly, for losses to be avoided, for appetite to stay aligned, for growth to build on discipline, for limits to guide decisions, for treasury and capital management to create value, for the investment function to contribute real economic return, for pricing to remain tight, for models to illuminate reality, for capital to be well allocated, for accounting to support true economics, for processes to be timely, and for frameworks to be holistic.

These outcomes are not coincidences. They arise from systems that are designed, connected, and governed for complexity.

But across the industry, these systems rarely exist in full. Insurers often rely on fragmented processes and misaligned functions: treasury acting without visibility into liquidity pathways, capital management operating on stale assumptions, investments pursuing return without ALM integration, pricing working with incomplete constraints, and accounting frameworks that distort rather than clarify economic value.

When this happens, insurers experience recurring patterns:

- appetite evaporates without clear cause

- frictional costs accumulate unnoticed

- limits become symbolic rather than binding

- pricing becomes too generous under pressure

- growth stalls despite market opportunity

- profitability erodes long before it appears in P&L

None of this is due to weak teams — the expertise exists everywhere.

The issue is that the system does not reflect the actual risks, frictions, constraints, and interdependencies of modern balance sheets.

This is the heart of ALM.

ALM is not a reporting function. It is the strategic engine that integrates:

- capital

- liquidity

- investment

- treasury

- accounting

- pricing

- market risk

When ALM works, it unlocks capacity, enforces discipline, strengthens pricing, reveals frictional costs, and turns complexity into navigable structure. When it fails, value is destroyed silently — in treasury flows, spread realism, liquidity constraints, reinvestment assumptions, and accounting artefacts. A modern ALM function must therefore be intentional, timely, integrated, explainable, and economically grounded.

That is the journey this article explores: how insurers can build systems that deliver the outcomes we know are possible — and avoid the failures we have all seen.

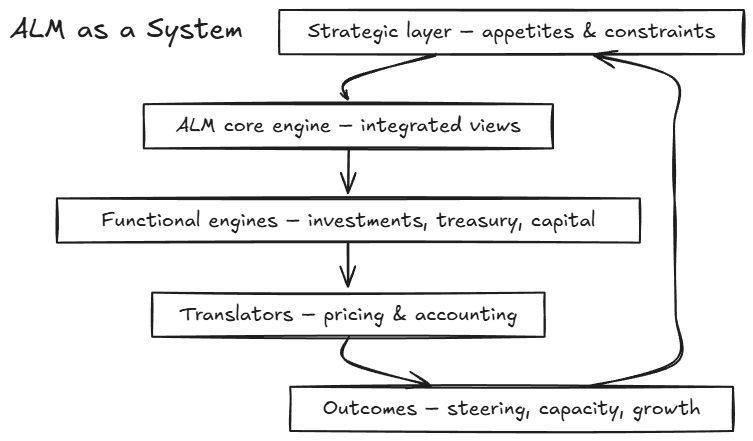

The ALM System — Overview

ALM must be understood as a connected system, not a department.

The diagram below illustrates this structure in a mobile-friendly format.

Figure: Strategy → ALM Core Engine → Functional Engines → Translators → Outcomes, with feedback loops that refine appetite and constraints.

To clarify the layers shown in the simplified diagram:

- Strategic layer: appetite and constraints

- Core engine: integrated economic, liquidity, capital and accounting views

- Functional pillars: investments, treasury, capital management

- Translators: pricing & accounting as constraint enforcers

- Outcomes: steering, capacity, growth, stability

- Feedback loop: outcomes refine appetite dynamically

Why Systems Win Where Processes Fail

Most insurers do not suffer from lack of intelligence or expertise. They suffer from disconnected systems:

- Treasury decisions that ignore investment flows

- Capital assumptions that lag economic reality

- Pricing frameworks unaware of liquidity constraints

- Investments managed without solvency context

- Accounting volatility shaping decisions more than economics

The ALM system binds these parts into a coherent whole — and coherence is what produces high-quality outcomes.

What a Modern ALM Engine Must Deliver

A functioning ALM system provides:

- Timeliness — decisions based on updated economic, liquidity and solvency conditions

- Integration — one coordinated model of risk, capital, liquidity and accounting

- Explainability — narratives that reconcile numbers with decisions

- Economic grounding — true value creation over accounting artefacts

- Strategic feedback — outcomes that refine appetite dynamically

ALM becomes active steering, not backward reporting.

The Value Case for Integrated ALM

With a modern ALM system, insurers gain:

- visibility of frictional costs

- discipline in pricing

- capital efficiency

- liquidity resilience

- clearer growth decisions

- reduced operational surprises

- transparency in risk and return

Without it, value disappears silently for years through cumulative structural leakage.

Conclusion

ALM is not about producing reports. It is about building systems that create clarity, capacity, and long-term value. Insurers who recognise this shift — and who design ALM as an integrated, feedback-driven engine — position themselves for sustainable profitability and disciplined growth.

Tags: ALM, insurance, capital-management, strategy